Beef cow and breeding heifer numbers on July 1 were down, indicating the beef industry is still in the consolidation phase. Heading into 2015 expansion is anticipated to be slow both north and south of the border.

DEMAND

The fundamentals that have driven the market higher throughout 2014 will remain supportive to prices. The big question for 2015 is going to be how much pressure will come from pork and poultry if they can expand production and reduce prices. If the beef industry retains heifers for expansion in 2015, production will be even lower. This will create price pressure and potentially have consumers move away from beef towards other proteins. At this point in the cattle cycle the critical piece is not to sell more beef (we don’t have it!) but to prevent the loss of domestic consumption which is really hard to gain back later.

Read Also

Canadian Beef Check-Off Agency reports on investments and activities

The check-off agency’s work behind the scenes is what ensures cattle check-off dollars are invested wisely, accounted for transparently and deliver measurable value back to producers and importers.

We typically focus on beef supplies in this article but this time we are going to take a closer look at consumers as retail prices have been record high and media coverage this summer has been extensive.

Consumer demand is strong

Supply is only half of the equation when looking at the cattle market. While we have good data on beef supplies both domestically and globally; demand is more of a mystery with most data sets lagged by several months. However, we can still say something based on consumer response in the first half of the year.

Beef supplies available for consumption are projected to be down around 4.5 per cent in 2014 with slightly smaller domestic production, smaller imports and larger exports. Deflated retail beef prices have made new highs each month, averaging 10% higher so far this year. The increase in retail prices is more than what would be expected with smaller supplies indicating that consumers are willing to pay more for beef. In other words beef demand will be up in 2014.

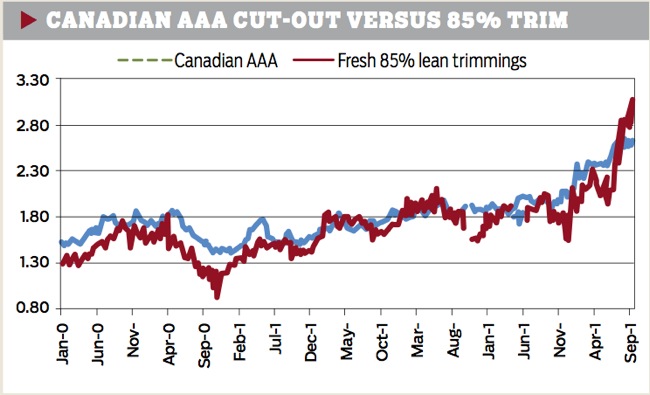

Further upward movement in retail beef prices is anticipated going into 2015. Why? The AAA cut-out jumped sharply higher from December 2013 to March 2014 (+16 per cent) before stabilizing. It then jumped higher again in June and July (+10 per cent) before stabilizing in August and September. Most food-service companies price their product needs just once or twice a year. As a result higher wholesale prices have yet to be fully passed on to the consumer. This will occur over the next several months. Consequently, strong wholesale and live prices reflect the market’s anticipation of future consumer demand. Knowing how demand will actually change going forward is extremely difficult to predict. The most accurate predictor of demand is seeing how consumers have responded in the recent past, which has been extremely positive so far this year.

International demand is also strong with the average per-unit export price up 20 per cent from January to August and volumes up 10 per cent. Exports have been supported by a lower Canadian dollar; but overall global demand remains exceptional and is not going away. The FAO Outlook for the next 10 years shows the largest trade deficits for beef will be in Asia and Europe. Import growth in Asia is driven by growing incomes, which is a key demand driver for beef. In Europe, declining production along with stable demand for high-value products and a strong currency will support future imports.

The competition is slow to expand as well

The strong rally in beef cut-out values this spring and summer was made possible by an equally impressive run-up in pork cut-out values as the impact of PEDv hit the market. In fact, the price relationship between beef and pork was maintained as both commodities moved higher and has only recently become strained as the pork cut-out drops. This eliminated much of the question about consumers switching between proteins. In addition, production increases in the poultry sector have been modest at best as it has also had issues with expansion.

The main competition over the next two to three years will be competing meats that are able to increase production faster than beef and therefore gain market share. The market is well aware that beef supplies are expected to get smaller while pork and poultry supplies will get larger over the next year. The question of how retail price relationships will be impacted depends on how well the pork industry is able to address PEDv this winter. Regardless, both pork and poultry expansion is anticipated to be slow in 2015. This will support the protein complex overall and the beef cut-out. Expect further prices increases throughout the spring.

SUPPLY

Canadian herd shows no growth

Total cattle inventories on July 1 were down 1.4 per cent at 13.3 million head after seeing a 0.1 per cent increase in 2013. Beef cow inventories were down 1 per cent or 40,900 head to 3.92 million head. Regionally, Alberta with the largest beef cow herd at 1.58 million head was down 1.3 per cent from last year, followed by Saskatchewan with 1.17 million head down 0.8 per cent; Manitoba with 458,400 head down 1.1 per cent; Ontario with 289,300 head down 0.7 per cent; and British Columbia with 194,100 head down 2.1 per cent. Atlantic Canada (+0.5 per cent) and Quebec (+0.3 per cent) were the only regions with more beef cows. Breeding heifers were down 3.5 per cent or 22,300 head to 616,200 head with the entire decline coming from the west (-4 per cent) while the East (+0.3 per cent) appears to be more stable.

Slaughter heifers and steers were down 2.2 per cent and 1.8 per cent respectively. When combined with the slightly higher on feed numbers, Canadian feeder and calf supply outside of feedlots were down 2.4 per cent or 140,690 head. Significant interest in feeders and calves from U.S. buyers will lead to stiff competition for feeders this fall, and create a further tightening of feeder supplies before January 1.

Lots of talk but little walk in the U.S.

USDA has reinstated its July 1 cattle inventory report. While there are no official survey-based statistics for 2013, estimates were compiled by the Livestock Marketing Information Center (LMIC).

As of July 1, U.S. total cattle inventories were down 1 per cent from 2013 and down 3 per cent from two years ago to 95 million head. Beef cows at 29.7 million head were down 0.5 per cent from 2013 and down 2.6 per cent from two years ago. Beef replacement heifers at 4.1 million head were down 2.4 per cent from 2012 and the LMIC’s estimate for 2013. This indicates little or no increase in replacement heifer inventories from two years ago despite red-hot breeding heifer prices reported. While there has been a lot of talk about heifer retention in the U.S. the only solid indications that producers are interested in stabilizing the herd is smaller cow marketings and a narrower steer-heifer price spread.

Cycle indicators

The female-to-male disposal ratio (slaughter + exports – imports of all classes of cattle) is the best indicator of whether the herd is declining or growing. At 1.05 females being slaughtered for every male, we remain firmly in the consolidation phase for 2014 as heifer retention has not made up for sustained cow marketings. Beef cow inventories on January 1, 2015 will be lower.

Heifer-to-steer slaughter ratio

The number of beef heifers retained for breeding on July 1 was down 3.5 per cent. Heifer marketings in 2014 are anticipated to be up 4.3 per cent compared to steer marketings which are projected to be down 2.5 per cent. The heifer slaughter ratio, providing the number of heifers marketed for every 100 steers, confirms that producers are not breeding heifers. In 2014, the ratio was up to 70 compared to a low of 63 in 2013 and a 20-year average of 68. It is unsurprising that bred heifer trade has remained thin. That may not change in 2015 if producers choose to develop heifers from within their herd versus purchasing outside genetics.

Cow supply

The beef cow culling rate remains disappointingly high, at a projected 13 per cent in 2014 compared to 14.3 per cent last year and the 20-year average of 11 per cent. Domestic cow slaughter is down a modest 5 per cent; while live exports are down 14 per cent. Regionally cow slaughter is down 6 per cent in the West and 3 per cent in the East; while exports are down 11 per cent in the west and 17 per cent in the East. Overall, cow marketings (domestic slaughter + exports) are projected to be down 8 per cent in 2014.

Cow marketings have been encouraged by record-high prices this year. Prices have been exceptional with Alberta D1,2 cow prices reaching a high of $125/cwt in August, up 55 per cent from 2013. In the U.S. cow prices have been trading at a C$3-6/cwt premium to Alberta in the third quarter compared to a C$13-17/cwt premium in the first quarter. This has eased the incentive to go south.

Manufacturing beef and prices

The decline in cow slaughter draws attention to the importance of lean manufacturing beef in the overall beef market and consequently cattle prices. There is generally an inverse relationship between non-fed (cow and bull) beef production and non-NAFTA imports. When non-fed production is small, non-NAFTA imports increase and vise versa. However, there is currently strong competition from emerging markets for manufacturing beef and declining world beef production. As a result while non-fed production has declined non-NAFTA imports have not increased correspondingly; leaving a deficit in the manufacturing market and supporting cow prices.

Less than 20 per cent of Canada’s beef production is non-fed, from cows and bulls. The U.S also has less than 20 per cent of production from non-fed animals. This is despite its proportionately larger dairy herd. In the U.S. 24 per cent of its cow herd is dairy; while in Canada 19 per cent of the cow herd is dairy. Fed production in the U.S. is supported by imports of fed and feeder cattle from Canada and Mexico.

North American manufacturing beef is sourced from cull cows, of course, but also from the end primals (chucks and rounds) taken from fed cattle. While supplies of manufacturing beef are tight due to reduced cow marketings and limited imports; a larger portion of the fed animal is being ground. Therefore, as manufacturing beef prices increase they are pulling the entire cut-out along with it.

Beef imports down

U.S. beef imports are projected to end the year up 20 per cent supporting overall lean beef supplies south of the border. In contrast, Canadian beef imports are down 19 per cent Jan.-Aug. and are projected to end the year down 12 per cent or 56 million pounds. In addition, non-fed beef production is projected to be down 55 million pounds resulting in a combined reduction of lean beef supplies around 111 million pounds. If imports don’t increase in the fourth quarter, the decline will be even larger than that. Lean 85 per cent trim prices moved sharply higher in July and were 43 per cent or $85/cwt higher than last year in August.

Imports from the U.S. are currently down 22 per cent while non-NAFTA imports are down 11%. With such strong international demand non-NAFTA imports are not expected to increase much in 2015. Exports are up 13% from Jan.-Aug. and projected to end the year up 10 per cent resulting in an improved net beef trade balance and smaller domestic supplies.

With no change in supply in sight, trim prices will remain supportive to cow prices in 2015, encouraging cow marketings. As cow marketings are not likely to see a significant drop in the short term, heifer retention has to increase in order for the Canadian herd to remain stable, let alone grow. And yet the opportunity cost of retaining heifers versus selling them is record high. Consequently, expansion will be very slow both north and south of the border over the next two to three years.

Feeder prices push feedlot break-evens higher

Break-evens will continue to increase this fall with strong feeder prices. The Canfax TRENDS report shows projected feedlot margins, based on the live cattle futures, will become negative by January 2015. However, the cash market is significantly above the hedgeable price. Margins based on cash prices show strong profits for this summer as fed prices increased steadily to peak in July. However, few fed cattle are being sold cash and a record number of yearlings were contracted this spring. Therefore current feedlots margins are probably overstated while margins are expected to decline heading into 2015 they won’t be as bad as the cash market shows if feeder cattle were contracted.

An attractive fed-feeder swap has kept feedlots current and carcass weights light throughout 2014 despite lower feed costs. But as feed prices make their bottom this fall further, support for the feeder market will need to come from fed cattle prices.