The fed and feeder cattle markets have been quite volatile over the past couple of months. Cattle producers have been overwhelmed with discussions to explain the recent price behaviour. On August 3, the U.S. Bureau of Labor Statistics reported that job growth during July was lower than expected. The live and feeder cattle futures dropped sharply on this news.

Usually, cattle analysts focus on supply and the number of cattle coming available. However, producers are now concerned about beef demand and have to learn about another set of market influences. I’ve received many calls from cattle producers over the past month asking about unemployment rates, interest rates, equity markets and consumer spending. How are all these factors related to the cattle market? The cow-calf producer in Saskatchewan needs to know how some executive’s decision in Santa Clara, California, to lay off 15,000 workers affects their income. These two people are worlds away but connected very closely. Hopefully, this article will shed light on the connection.

There are four phases to the business or economic cycle. These include contraction, trough, expansion and peak cycles. The peak phase of the business cycle is followed by the contraction phase. At the end of the peak phase of the business cycle, interest rates are high and the unemployment rate is low. When the economy moves through the contraction phase or a slower growth period, interest rates start to decline as the unemployment rate increases. When unemployment rates increase, beef demand tends to soften or even decrease. The central bank’s purpose is to balance the goal of price stability (inflation) and healthy employment levels.

Let’s look at two examples. The U.S. Federal Reserve’s interest rate peaked in June 1981 at 19.1 per cent. At this time the unemployment rate was at 7.6 per cent. The economy started to contract and during the major recession of 1982, gross domestic product (GDP) was negative each quarter. The jobless rates started to increase in the fall of 1981 and peaked in December 1982 at 10.8 per cent. By December 1982, the U.S. Federal Reserve’s benchmark rate was at nine per cent. The U.S. Federal Reserve decreased its interest rate as the jobless rate increased through the recession.

In July 2007, the Fed Funds rate was at 5.26 per cent which was the high before the Great Recession. At the same time, unemployment was at 4.7 per cent. The main recession occurred from the fourth quarter of 2008 to the first quarter of 2009. In October 2008, the Fed lowered its policy rate to zero per cent. Unemployment peaked at 10 per cent in November 2009. We all remember how the cattle market behaved during the Great Recession.

It takes 12 to 18 months for interest rate adjustments to work through the economy. There’s a time lag and don’t forget this. The U.S. Federal Reserve’s benchmark rate in August was 5.5 per cent. At the time of writing this article, financial analysts were expecting an interest rate cut of 25 basis points on September 18. U.S. jobs data for July showed that U.S. employers hired only 114,000 Americans. This was lower than the 12-month average of 225,000 positions. From July 29 to August 5, the live cattle futures dropped nearly $10 as the industry was bracing for a poor jobs report.

Read Also

Factors influencing cattle feeder market during the fall of 2025

Market analyst Jerry Klassen weighs in on live cattle markets

Job growth will slow even further in upcoming months, causing beef demand to soften or even decrease. Lower demand will result in lower cattle prices. Average U.S. and Canadian consumers are cutting back on spending after 2.5 years of elevated inflation and one year of higher interest rates. On August 1, Intel announced it was laying off 15,000 employees just before the negative jobs report on August 3. The U.S. and Canadian economy will go through a period where unemployment levels increase. The Canadian economy lost 41,000 full-time jobs in the second quarter of 2024. McDonald’s sales slowed in the second quarter of 2024 and this is a leading indicator of the economy and beef demand.

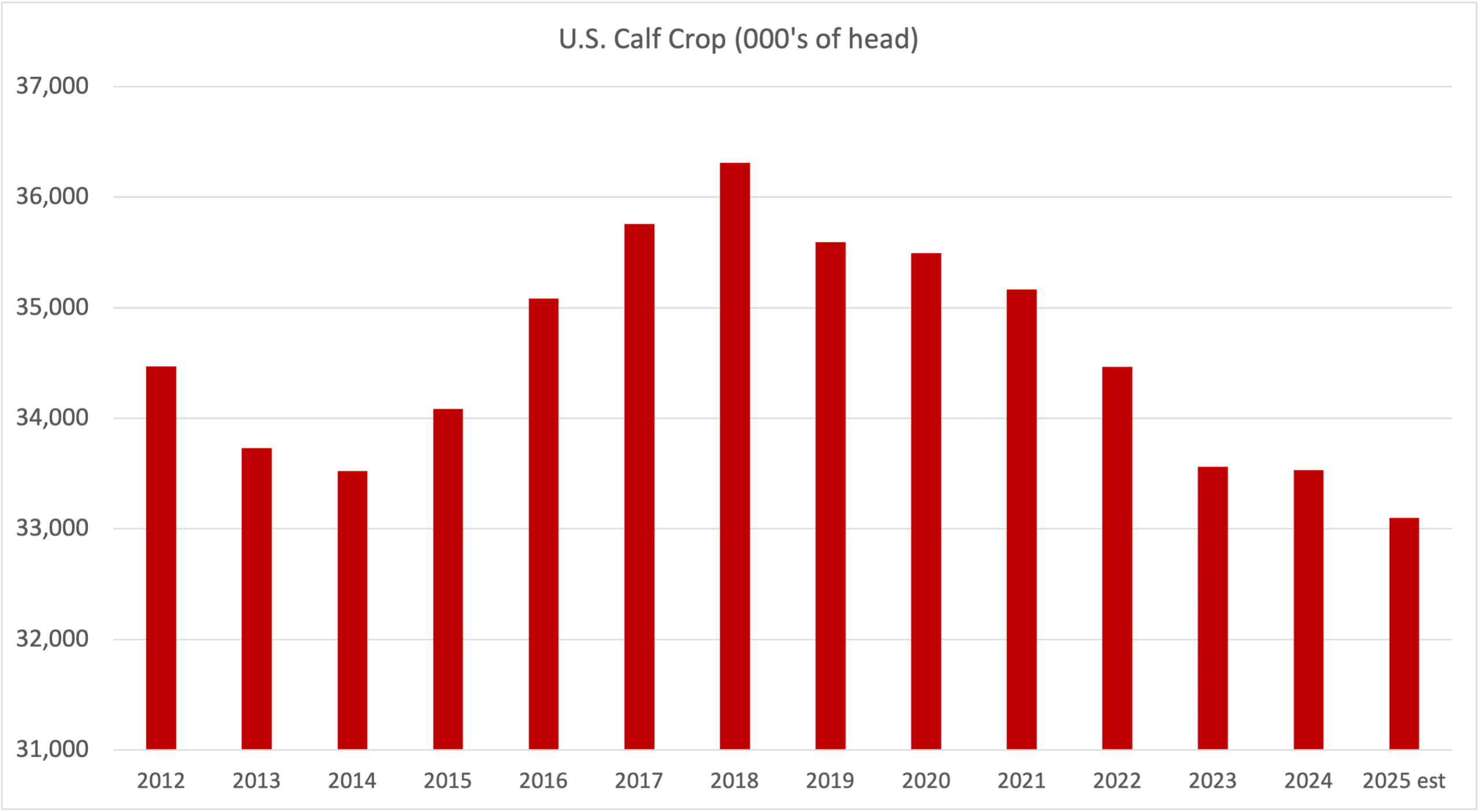

Another point to consider is that U.S. and Canadian cow-calf producers start expanding the herd when interest rates are at the roof. Back in 1981, U.S. cattle producers expanded the herd until 1983. The U.S. beef cow slaughter during June 2024 was 227,900 head, the lowest since July 2017. The U.S. cattle herd was expanding from 2016 through 2019. Cattle prices have been at or near historical highs for nearly two years, so the timing is correct for expansionary behavior. However, I’m only expecting a year-over-year increase in the calf crop in 2026. It takes a couple of years, after the cow slaughter decreases and heifer retention begins, for the calves to come on the market.

In conclusion, the unemployment rates on both sides of the border are expected to increase. The central banks will respond by decreasing their benchmark interest rates. Higher unemployment levels tend to result in lower beef demand as consumer spending decreases. History tells us that cow-calf producers expand the herd when interest rates reach the highs.