All wealth that flows to the U.S. beef industry comes from consumers at home and abroad. How much they are prepared to spend on beef largely determines whether packers, cattle feeders and producers make money or not. It is thus extremely important to monitor beef demand at retail and food service.

Beef demand was strong throughout 2023 despite an increase in retail beef prices and overall food inflation. Many market analysts believed that demand would begin to suffer this year because retail prices remained at or close to record levels. USDA’s latest monthly retail beef prices showed that its All Fresh retail beef price in May reached a new all-time high of US$7.96 per pound. It was up one cent from the April price and was up 6.1 per cent from May last year. Conversely, the May Choice price averaged US$8.11 per pound, down four cents from April and up only 0.5 per cent from May last year. The record-high All Fresh price in part reflected the high price of ground beef and beef patties.

The industry entered June knowing that the best demand month of the year was behind it. In addition, it faced the start of the so-called dog days of summer, which usually means a decline in beef sales because high temperatures force more Americans to stay indoors and eat cold cuts rather than grilling outside. The dog days normally do not start until July. But they came early this year as a blistering heatwave in mid-June extended from the Midwest to New England.

Read Also

Factors influencing cattle feeder market during the fall of 2025

Market analyst Jerry Klassen weighs in on live cattle markets

Yet the heatwave appeared not to affect beef sales. It certainly did not affect boxed beef cutout values. The national comprehensive cutout (cuts, grinds and trim) increased the week ended June 21 by US$6.19 per cwt from the prior week. The average of US$316.38 per cwt was the highest of the year. Also of interest was that the week saw the price of domestic lean manufacturing beef (90 chemical lean) set a new record of US$364.14 per cwt for the sixth week in a row. This was far above the Choice cutout, which averaged US$316.19 per cwt.

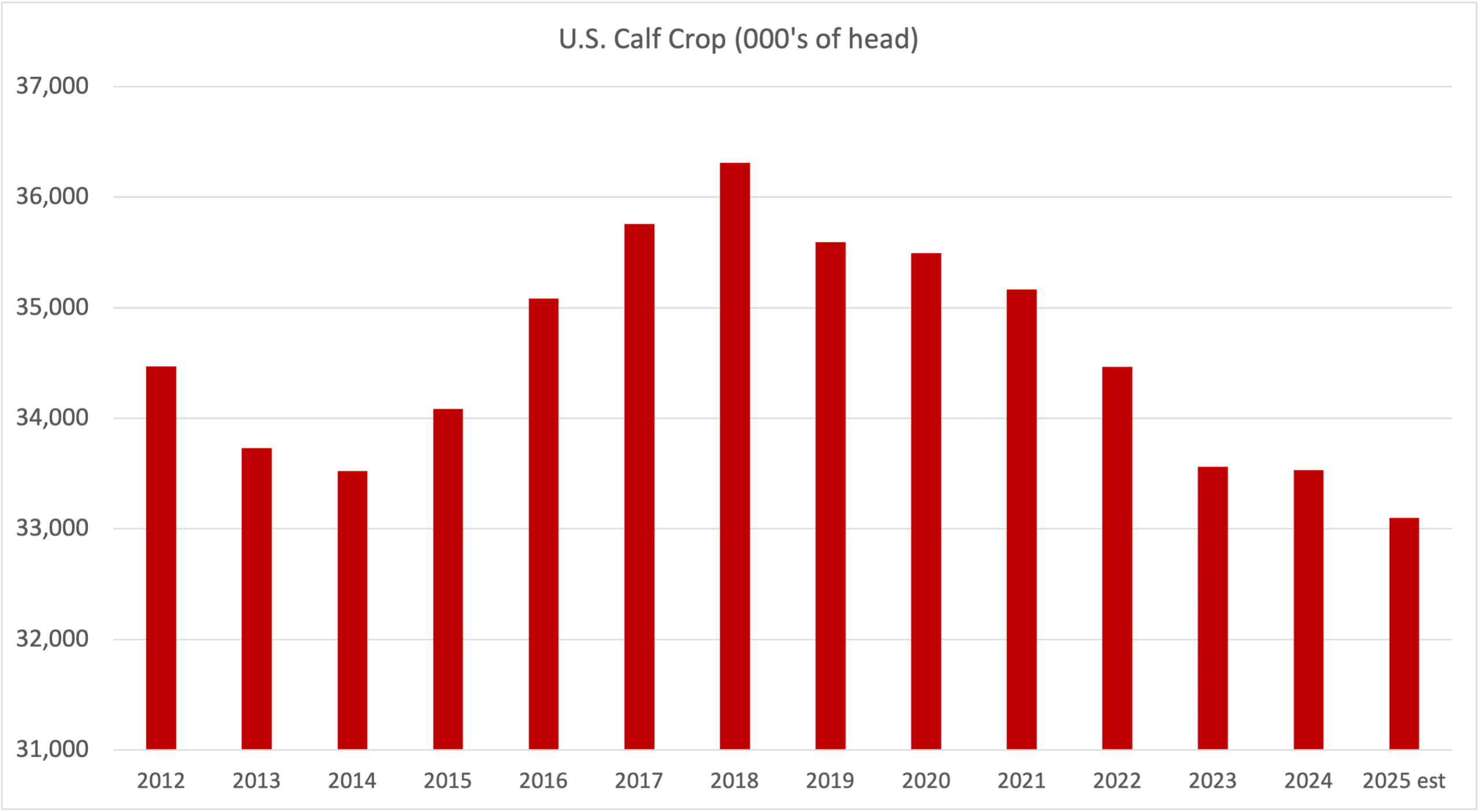

This partly reflects the fact that at the current harvest rate, annual cow slaughter is projected to decline by 962,695 head, according to Andrew Gottschalk of HedgersEdge.com. Beef cow harvest this year is estimated to decline by about 516,165 head from last year’s level, he says. It is interesting that to date, there is no decline in year-over-year heifer harvest. As heifer withholding for breeding begins, this would entail a further reduction in the level of annual beef production and in the available feeder cattle and calf supply for feedlot placement. These factors should lend additional price support to feeder cattle and calves on any price correction, he says.

Another positive in the live cattle market is that packer margins returned to being positive at the start of June after being negative every week this year but one. HedgersEdge.com calculated that margins the week before last were positive by US$32.79 per head, the highest of the year.

Latest USDA data meanwhile reveals that fed beef processors will enjoy ample supplies of live cattle through the rest of the year. That’s because front-end fed cattle supplies (on feed 150 days or more) are projected to remain above prior year levels through December unless there is a significant increase in the rate of marketings, says Gottschalk. How live cattle prices perform will depend on demand at home and abroad. The industry will be hoping that export sales pick up, as so far this year volume is well below that of last year.