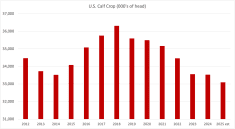

The Canadian beef cow herd appears to be in consolidation as liquidation has stopped, with reduced cow marketings. This phase of the cattle cycle typically lasts one to three years (with producers both entering and exiting, stabilizing and expanding) before true expansion begins. Carcass grading dipped slightly from last year but has been largely steady with a year ago since May. All classes of stockers, feeders and fed cattle have put on an impressive rally in the second and third quarters, in some cases, bucking seasonal trends. The Mexican feeder supply into the Southern Plains is shut off, with USDA projecting no feeder cattle trade through 2026. Year-to-date, beef export volumes are down, but the value is larger than last year and is expected to end the year at a record high. Beef imports remain elevated, both in volume and value.

Consolidation may be underway

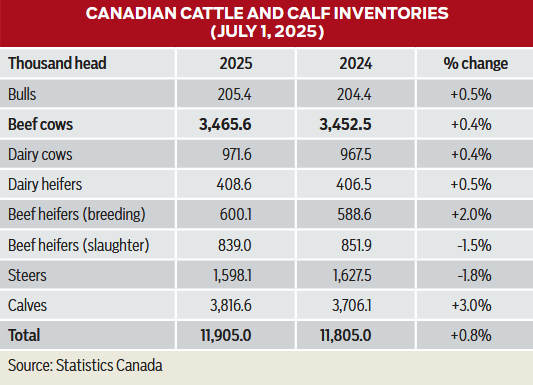

For at least the past two years, higher calf prices have pointed toward expansion of the Canadian beef herd. However, there have also been limiting factors, including depleted forage stocks and summer moisture. It should be noted that during the consolidation phase, which typically lasts one to three years, inventories move largely sideways, being up or down one per cent. Statistics Canada’s survey-based mid-year Canadian cattle inventory report shows modest increases in beef cow numbers (+0.4 per cent), with all provinces and regions showing an increase, except Alberta. The largest increase was noted in British Columbia (+2.7 per cent), possibly reflecting herd rebuilding after the devastating wildfire season in 2023. Other notable increases were Ontario (+1.1 per cent), Manitoba (up one per cent), and Saskatchewan (+0.5 per cent).

Read Also

Coronavirus vaccine reduces respiratory disease treatments in beef calves

A clinical trial on 887 calves tested whether intranasal bovine coronavirus vaccination at birth could reduce respiratory disease treatments.

This generally optimistic tone also rippled into the heifer category. Beef heifers retained for breeding were up two per cent nationally with all provinces/regions seeing an increase. The largest increases were in Saskatchewan (+2.7 per cent), Alberta (+1.9 per cent) and Quebec (+1.8 per cent), with smaller gains in Ontario (+1.1 per cent) and Manitoba (up one per cent).

Both steers (-1.8 per cent) and slaughter heifers (-1.5 per cent) were down from last year. Calves under one year old were up three per cent, though some of this increase was due to Statistics Canada revising the 2024 calf crop down by almost 60,000 head. The smaller 2024 calf crop (down 154,000 head from 2023) has contributed to tight third-quarter 2025 fed cattle marketings.

According to Agriculture and Agri-Food Canada, large areas of Western Canada — including the northern half of Alberta and Saskatchewan, most of Manitoba, and parts of Ontario and Quebec — are under varying degrees of drought conditions, ranging from abnormally dry to extreme drought as of the end of August. As of August 31, approximately 70 per cent of Canada’s agricultural land was located in areas experiencing drought. Looking a little deeper at regional agricultural landscapes, 89 per cent of the Pacific region, 59 per cent of the Prairie region, 84 per cent of the Central region, and 100 per cent of the Atlantic region were under either abnormally dry (D0) or drought (ranging from D1-D3) conditions at the end of August.

U.S. cattle herd looks for a bottom

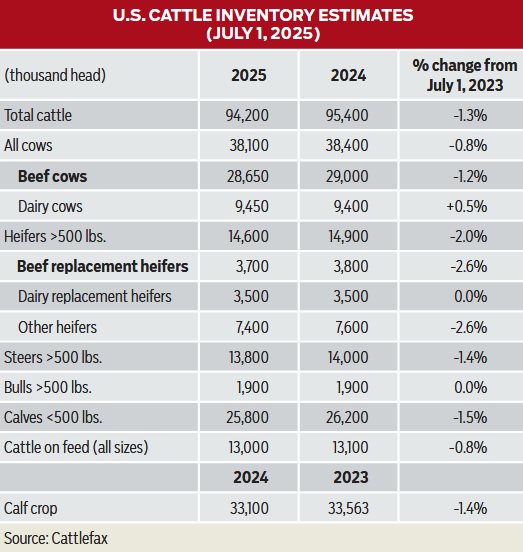

The USDA July 1, 2025, cattle inventory report showed total cattle and calves down 1.3 per cent from 2023 (due to no report in 2024). Declines were noted across most classes, including beef cows ( -1.2 per cent), beef heifers retained for breeding (-2.6 per cent), steers over 500 pounds (-1.4 per cent), other (a.k.a. slaughter) heifers (-2.6 per cent), and calves under 500 pounds (-1.5 per cent). Only dairy cows (+0.5 per cent) were higher than in 2023. Dairy replacement heifers and bulls over 500 pounds were steady with the 2023 report.

At the time of the release in late July, approximately 71 per cent of cattle located in the continental U.S. were in areas that were reported to be drought-free. By mid-September, approximately 49 per cent of cattle were located in drought-free areas. The percentage of cattle located in drought-free areas is the largest for mid-September since 2020.

Tighter U.S. feedlot supplies continue to be a reality, especially for southern feedlots, as New World screwworm affects live cattle imports. January to July feeder imports from Mexico were 214,000 head, down 75 per cent from the same period last year and down 70 per cent from the five-year average. U.S. Agriculture Secretary Brooke Rollins closed the U.S. border to livestock imported from Mexico on July 9, 2025, citing the resurgence of New World screwworm that appeared to be eluding containment efforts. Previously, the border was closed in late November 2024 but reopened under stringent oversight and monitoring in February 2025. This lasted until mid-May when screwworm threats into the U.S. were renewed. Another attempt at opening the southern U.S. border was made in July. However, this only lasted a couple of days before closing again.

In June, Secretary Rollins announced a five-pronged approach to combat this pest. As of mid-August, USDA’s Foreign Agricultural Service projected live imports of Mexican feeder cattle for the remainder of 2025 and 2026 would be zero.

Year-to-date, feeder imports from Canada are just over 100,000 head, up four per cent from last year and up four per cent from the five-year average.

Canadian steers lighter, heifers heavier

Canadian steer carcass weights followed in line with seasonal trends through the spring and into the summer of 2025. Carcass weights in April and May were stable with the five-year average. Since June, they have been slightly heavier than a year ago.

Heavier heifer carcass weights were recorded every month except February. Heifers moved counter-seasonally heavier from March right through May, topping just shy of 880 pounds before seasonally declining in June and July. At their heaviest, heifer carcasses were 37 pounds above both last year and the five-year average.

Through the first half of September both steer and heifer carcass weights were heavier than both last year and the five-year average, as cheaper cost of gain encourages days on feed.

Heifer placements as a percentage of total placements into Alberta and Saskatchewan feedlots were below both last year and the five-year average in August. Heifers placed as a percentage of total placements were below both last year and the five-year average every month since March, with the exception of June when it spiked to be above both historical markers. There have been reports that more heifers have been retained on cow-calf operations, keeping them out of the slaughter mix, as producers get set to rebuild herds.

Year-to-date, carcasses grading either AAA or Prime accounted for 77 per cent of all youthful carcasses, down slightly from 77.5 per cent during the same period last year. Carcass quality through the hot summer months has been mostly steady with last year and above the five-year average.

With retail prices at or near record highs, it is important to maintain quality grading to provide consumers with a consistent eating experience and support beef demand. Greater marbling is more forgiving in the kitchen for those with less cooking experience.

Domestic fed production steady, non-fed lower

Year-to-date, domestic beef production (to the week ending September 14) was down five per cent from last year and down seven per cent from the five-year average. Similar declines were noted in fed production: down five per cent and down seven per cent, respectively. Largely mirroring fed production, non-fed production was down four per cent from last year and down seven per cent from the five-year average. So far this year, there have only been two months where monthly production was higher than last year. The first was in April due to an additional week in 2025 and the second was in June due to the Cargill Guelph packing plant shutdown in 2024 due to a labour strike.

Canadian export volumes pull back, values increase

From January to July 2025, beef export volumes were down five per cent from last year and down a slight one per cent from the five-year average. Based on current data, Canada is projected to export 471,000 tonnes of beef in 2025. If projections hold, this will be the smallest volume exported since 2020.

The top five export markets for Canadian beef, by market share, are the U.S. (73.9 per cent), Japan (9.2 per cent), Mexico (7.1 per cent), Southeast Asia including Taiwan (3.5 per cent) and South Korea (3.3 per cent).

Year-to-date, the value of Canadian beef exports is up a moderate six per cent from last year. Based on January to July data, export values are projected to be $5.2 billion in 2025. Furthermore, export values are projected to be the largest on record and only the second time that values have crossed the $5 billion mark.

By value, the top five export markets are the U.S. (77.5 per cent), Japan (7.6 per cent), Mexico (6.5 per cent), South Korea (3.3 per cent) and Southeast Asia (three per cent).

Live exports drop

From January to July, live slaughter exports were down eight per cent from last year but up eight per cent from the five-year average. In the West, slaughter exports were down 10 per cent from last year and down one per cent from the five-year average. Meanwhile in the East, slaughter exports were down four per cent from last year but up 32 per cent from the five-year average. Live slaughter exports in the first quarter were up 58 per cent in the East and up 12 per cent in the West as producers looked to market their cattle into the U.S. in advance of tariff threats. Between April and July, slaughter exports dropped to be 31 per cent below a year ago in the West and were down 35 per cent in the East.

Fed prices roar higher

Alberta fed steers averaged $304/cwt in August, up $54/cwt from last year and $114/cwt above the five-year average. Ontario fed steers averaged $315/cwt in August, up $66/cwt from last year and $120/cwt above the five-year average.

There has only been one time in the past 50 years that Alberta fed steers established annual highs in August. Furthermore, annual highs have never been established in September. This summer looked to be the second occurrence where annual highs would be established in August. However, continued strength over the first three weeks of September may be another feather in the cap for a fed market that has continued to defy expectations.

There may be a case made that the Alberta fed market has been underperforming against their regional counterparts, even as it establishes new all-time highs on an almost monthly basis. Alberta fed steers were, on average, at a $14/cwt discount to the Ontario market between June and August and a C$25/cwt discount to U.S. fed steers (all area average).

Lean trim prices support cull market

Lean trim prices continue to support the cull cow market. Lean 85 per cent trim has moved higher every month since April, topping near US$400/cwt in August. Ontario D2 cow prices have moved very similarly to lean trim prices, climbing higher every month since March. Ontario D2 cows continually re-established new highs between May and August. By August, Ontario D2 cows averaged $222/cwt. Alberta D2 cows also had a stronger market tone during the first half of the year, topping at $229/cwt. July and August brought some headwinds to the Alberta cull cow market, with prices softening to just under $220/cwt. Alberta D2 cows were at a premium to both the Ontario and U.S. markets between April and June but moved to be at a discount to both regions by August.

Feed grain prices ease lower into harvest

An anticipated record U.S. corn crop is weighing on the Alberta barley market. Omaha corn peaked in April near US$4.65/bu and has been declining in the months since. Since the June high, Lethbridge barley has softened 12 per cent to around $283/tonne by August. A continued softer tone has been noted into September, with Lethbridge barley prices near the $270/tonne mark. Ontario corn has been on a steady decline since April, softening nine per cent by August to $224/tonne. Both Lethbridge barley and Ontario corn prices were at or below their respective 10-year averages in August.

In August, Lethbridge barley was up seven per cent from last year, Ontario corn was up eight per cent, but Omaha corn was down three per cent.

Feeder prices on fire

Feeder cattle in both Alberta and Ontario have had an optimistic tone to their markets in 2025. A notable move higher began for Alberta steers 700 pounds and over beginning in April, with little sign of slowing down. Their lighter-weight western Canadian counterparts were more muted in their rally until July, when they shot higher, making up for lost time.

In Ontario, all classes of feeder cattle began to move higher in April, once the market was assured that tariffs would not be levied on USMCA-compliant products, including live cattle and beef exports (with the exception of a few days at the beginning of April). Most classes of Ontario feeder cattle took a breather in June but continued their climb in July and August.

From a historical perspective, the feeder market tops in August or September as the fall run ramps up. However, with the U.S.-Mexico border closed through the remainder of 2025 and all of 2026, the North American feeder market has been red-hot and may experience price corrections as it finds a new trading range. Canadian cow-calf producers may have also begun to retain some of their heifers for replacements, reducing the pool of cattle that feedlots can pull from, possibly providing additional support to the feeder market this fall.

Ontario 550-pound steer calf prices were at a premium to both Alberta and the U.S. between May and July, while their heavier-weight 850-pound counterparts have been the premium market since April. During the first half of September, Alberta 550-pound steers were once again the premium North American market while 850-pound steers were at a premium to the U.S. but at a discount to Ontario.

Replacement ratios record high

Replacement price ratios measure the price of a feedlot replacement animal purchased against the price received from an animal sold on a per-hundredweight basis. This ratio also plays an important role in profitability as more dollars required to pay for a replacement animal leaves fewer dollars available for other expenses and can reduce margins.

Price ratios were record-high in the third quarter of 2025 for all classes of cattle in both Alberta and Ontario. Price ratios widened 10-15 per cent in the East and 15-24 per cent in the West on steer and heifer calves compared to the third quarter of 2024. Yearling price ratios widened seven to 10 per cent in the East and 12-17 per cent in the West in the third quarter of 2025 compared to a year ago.

Risk management strategies are key to reduce feedlot debt exposure as the price cycle rallies.