I’ve received many calls and emails over the past month from cow-calf producers inquiring about the price outlook for feeder cattle prices this fall. At the time of writing this article in late July, 975-pound yearling steers off grass were trading for $430/cwt. Calf prices have jumped sharply throughout the summer and we now find 500-pound steer calves edging towards $700/cwt. Feedlot margins have been in positive territory throughout the spring and summer. It appears that there will be equity building in the feedlot sector over the next couple of months. In this article, I will discuss four main factors influencing the price of calves and yearlings during the fall period.

Feed grain prices are expected to trend lower during the fall period. Production forecasts for Canadian barley and U.S. corn are larger than earlier projected. We’re now expecting the Canadian barley crop to reach nine million tonnes, up from the 2024 harvest of 8.1 million tonnes. U.S. corn production estimates range from 410-415 million tonnes, up from the 2024 crop size of 378 million tonnes. U.S. corn has potential to trade into southern and central Alberta from November 2025 through July 2026. Barley and corn prices are set to drop $30-$40/tonne, which will lower the cost-per-pound gain for feedlot operators in Western Canada. The corn and barley markets will function to encourage demand through lower prices. This will be supportive for the feeder market during the fall and winter.

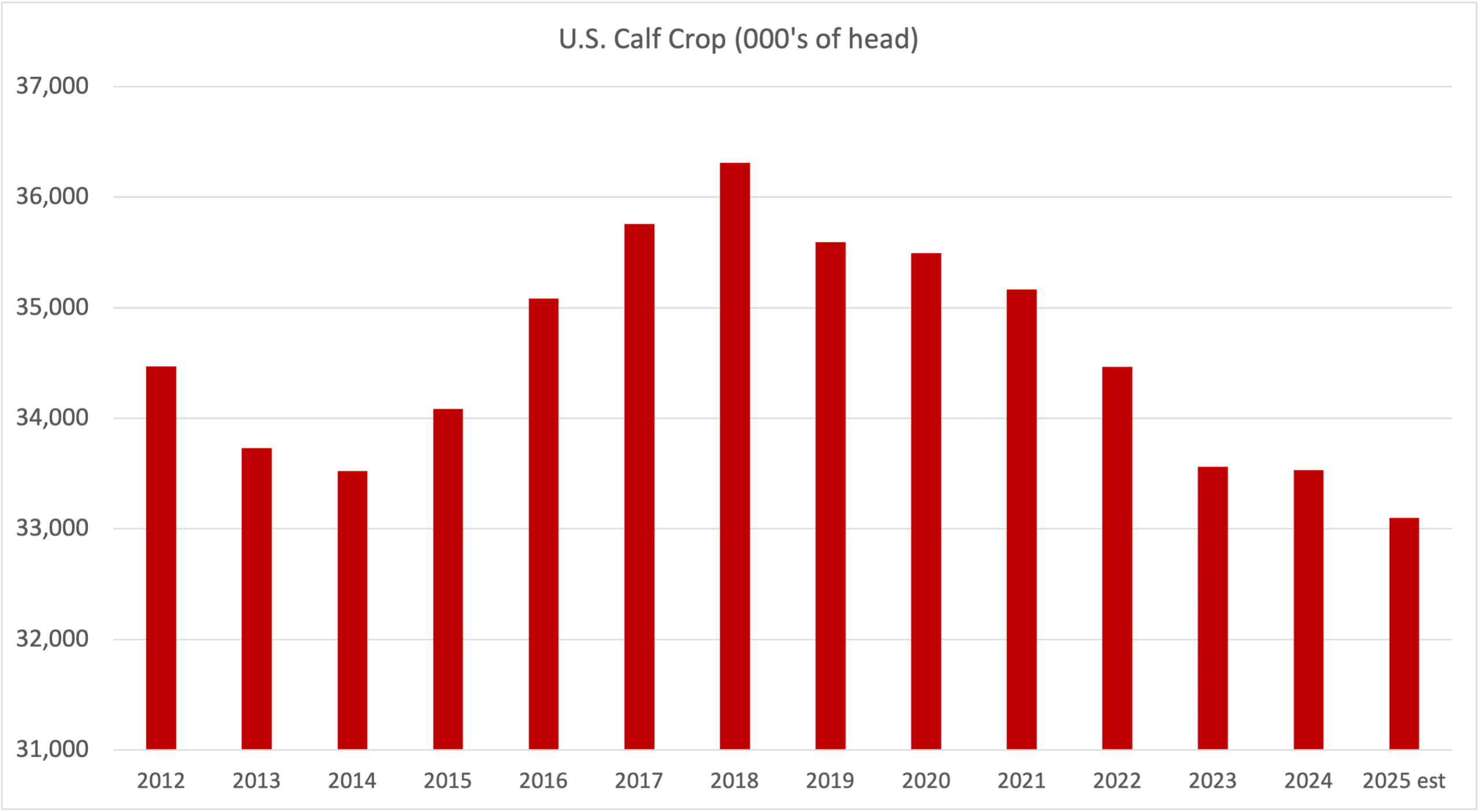

Secondly, the fundamentals for feeder cattle remain historically tight. The USDA’s Semi-Annual Cattle Inventory Report showed that the U.S. cattle herd remains in a contraction phase. The 2025 U.S. calf crop was estimated at 33.1 million head, down 429,000 head from the 2024 calf crop of 33.529 million head. The behaviour of the Canadian cow-calf producer usually mirrors their U.S. counterparts. We’ll likely see a year-over-year decrease in the 2025 Canadian calf crop.

Read Also

Cattle Market Summary

Break-evens, cow and calf prices, plus market summaries courtesy of Canfax and Beef Farmers of Ontario. Cost of Production October…

There has been a record number of calves and yearlings sold for fall delivery in the U.S. and Canada. Usually, auction market volumes make seasonal highs during October and November. This year, the number of feeder cattle coming on the market in the final quarter of 2025 will be down from last year. This year-over-year decline in feeder cattle numbers may be a surprise to the market.

According to the USDA, U.S. fourth-quarter beef production is expected to finish near 6.605 billion pounds, down 275 million pounds from the same period of 2024. U.S. 2026 first-quarter beef production is expected to dip to 6.36 billion pounds, down 183 million pounds from the first quarter of 2025. Lower U.S. beef production in the fourth quarter of 2025 and the first quarter of 2026 is expected to enhance fed cattle prices on both sides of the border. I’m expecting the February and April 2026 live cattle futures to incorporate a risk premium due to the uncertainty in production. This is the third main factor underpinning the feeder market in the fall of 2025.

Finally, U.S. and Canadian beef demand has been stronger than expected. Normally, when wholesale and retail beef prices are at historical highs, demand would start to decline. However, we’re seeing an abnormal economic environment for beef in 2025. Analysts can make the argument that beef demand is actually higher on a per-capita basis. U.S. restaurant traffic has been running eight to 10 per cent above year-ago levels in July. Canadian restaurants have experienced a year-over-year increase of 20-25 per cent.

There are several reasons for the increase in demand. The U.S. economy is running on all cylinders. Ongoing job and wage growth have contributed to higher income levels for the average American. There also appears to be a change in tastes. There is a fad in the U.S. to eat more red meat for weight-loss purposes. The “keto diet,” for example, encourages participants to eat more red meat. There is also the “carnivore diet’ made famous by certain celebrities. The Canadian economy is experiencing a recession, but this hasn’t curbed restaurant demand. Canada is receiving the benefit of larger tourism spending. Canadians are staying at home while Europeans and Asians are coming to Canada instead of the U.S. Grocers often use beef as a loss leader to attract customers into the store. The general public may be receiving a benefit for this reason, as steaks and ground beef are priced below full value.

In conclusion, the feeder cattle market is expected to percolate higher throughout the fall period. Feed grain prices are expected to drop by $30-$40/tonne over the next month. The U.S. and Canadian cattle herds remain in contraction. Beef production will be down sharply in the fourth quarter of 2025 and the first quarter of 2026. Beef demand has remained constant or even increased despite the historically high prices in restaurants and grocers. This is a new market environment for the feeder cattle market. c