Live and feeder cattle futures dropped sharply in early August. While the supply fundamentals for the cattle market hadn’t changed, the cattle futures started to incorporate a risk discount due to the uncertainty in demand. Consumer confidence appears to be decreasing and job growth has slowed. Restaurant spending made seasonal highs in June and recent data shows that Americans and Canadians are pulling in the reins on discretionary items. McDonald’s for example, reported that U.S. same-store sales decreased 0.7 per cent during the April through June quarter. This compares to growth of 10 per cent in the same quarter last year. The U.S. and Canadian central banks have been trying to achieve an economic “soft landing.” This involves increasing interest rates to bring down inflation without causing massive unemployment and a recession. The economy is now close to landing as inflation nears the two per cent target but it could be harder than earlier anticipated. Consumer spending will decline moving forward and this will result in lower beef demand.

U.S. inflation moved above two per cent year-over-year in March of 2021 and peaked at 9.1 per cent during June 2022. The U.S. Federal Reserve started increasing their policy rate in March 2022 and continued to make 11 increases of various size so that the benchmark rate was in the range of 5.25 per cent to 5.5 per cent on July 31, 2023. The U.S. central bank has held interest rates at this level for one year with no changes at the meeting on July 31, 2024. U.S. inflation was reported at three per cent this past June. Recent price data suggests that U.S. inflation could be near two per cent by the end of 2024.

The Bank of Canada also started to increase its interest rate in March 2022. On July 12, 2023, the Bank of Canada made their final increase resulting in a policy rate of five per cent. On June 5, the Bank of Canada made their first interest rate cut of 25 basis points which was followed by another cut of 25 basis points on July 24. The Canadian Consumer Price Index moved above two per cent in March 2021 and peaked at 8.1 per cent in June 2022.

It’s important to note that it takes 12 to 16 months before interest rates are fully implemented into the economy. During the second quarter of 2024, Canada lost 41,000 full-time positions. U.S. employers added 532,000 jobs in the second quarter but recent data shows that there were only 100,000 jobs added during July. This is down sharply from previous months. More importantly, wage growth is slowing. The economy is starting to experience the effects of higher interest rates. Canadians have a more difficult time because many households are in the process of renewing four or five-year mortgages.

This next point is very important. The “Sahm Rule” states that, when the three-month moving average of the unemployment rate exceeds the lowest unemployment rate of the last 12 months by more than 50 basis points, economists can expect lower growth. In June, the U.S. unemployment rate rose to 4.1 per cent, causing the three-month moving average to rise to four per cent. The lowest unemployment rate of the last 12 months was 3.5 per cent. The job market is loosening and wage growth is slowing. This “Sahm Rule” has held water for the past 60 years. Economists are expecting slower growth and lower corporate earnings over the next 12- to 16-month period. This will result in layoffs. I’m not saying to be prepared for a recession, but beef demand will decline. There is no doubt about it.

Read Also

Factors influencing cattle feeder market during the fall of 2025

Market analyst Jerry Klassen weighs in on live cattle markets

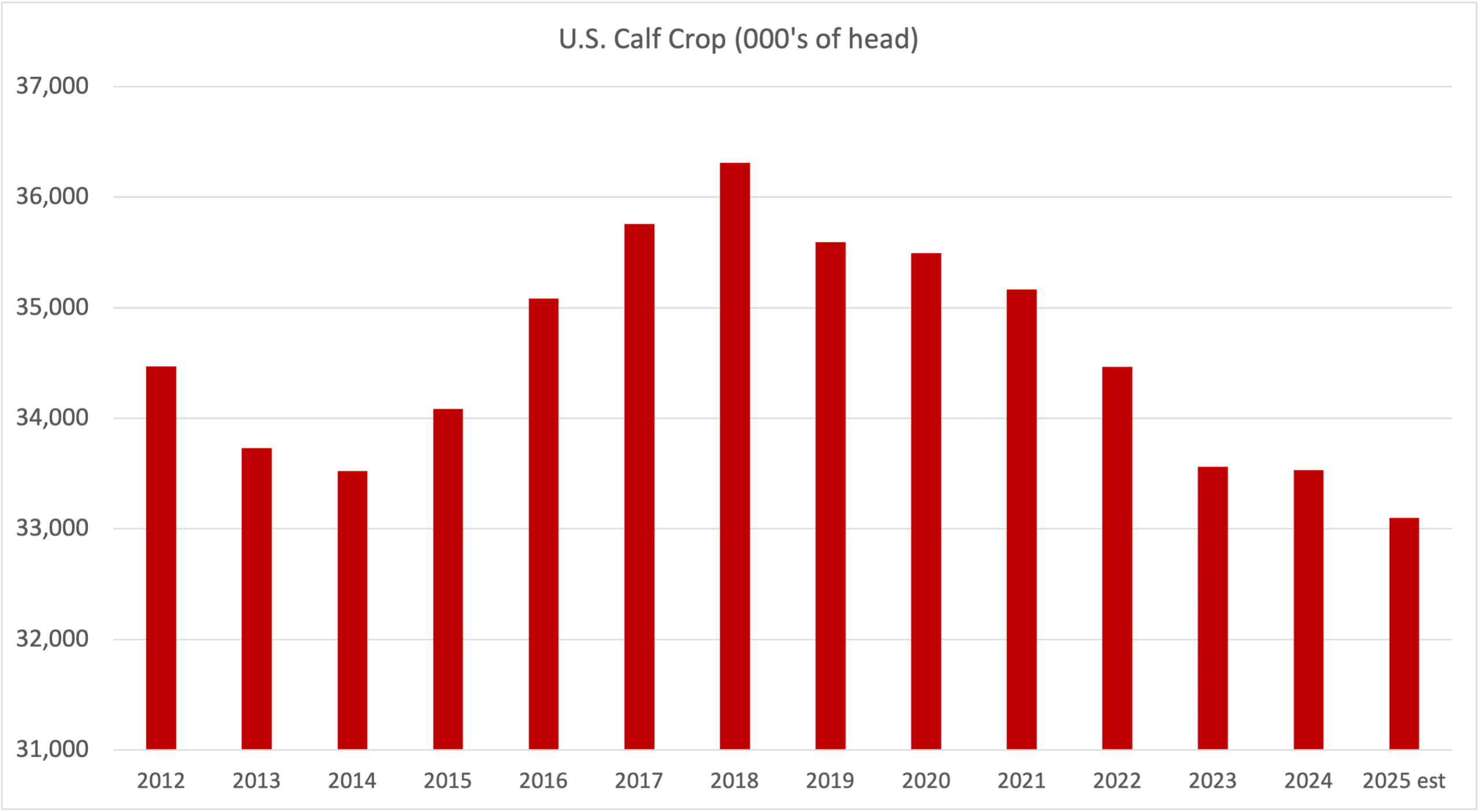

I’ve mentioned in the past that as a rule of thumb, a one per cent increase in consumer spending equates to a one per cent increase in beef demand and vice versa. Consumer spending comprises about 70 per cent of U.S. gross domestic product (GDP). If U.S. GDP is not above two per cent, the cattle market tends to trend lower. U.S. GDP in the third and fourth quarters of 2024 is expected to average one per cent, which may be optimistic. U.S. and Canadian consumers are in a difficult situation. Inflation growth has come down but prices for necessities remain elevated. Prices for many goods and services are higher than last year and these costs are not dropping anytime soon. Cattle producers can expect that if the U.S. GDP remains below two per cent for an extended period, the cattle market will trend lower for the same amount of time. We probably have lower prices from the third quarter of 2024 through the first quarter of 2025. There will be three quarters of soft economic growth.

The live cattle futures have been in an upward-trending market since the lows of 2020. Technically, when a market breaks a long-term upward trend, there is usually a significant move to the downside. Take precautions!