It’s that time of year when I receive many inquiries about the feed barley outlook. During late June and early July, feed barley in the Lethbridge area was trading in the range of $285/mt to as high as $300/mt. At the time of writing this article in early September, feed barley was trading from $210/mt to $220/mt delivered in southern Alberta, and $195/mt to $205/mt in central Alberta. The price of feed barley has dropped over $80/mt within a two-month period.

Feedlot operators are now asking whether the market has further downside potential or if they should be booking their forward requirements. On the flip side, lower feed grain costs have contributed to strength in yearlings. Cow-calf operators are asking if these prices are here to stay or if barley prices will rally over the winter and pressure the feeder market. Therefore, I thought this would be an opportune time to review the fundamental structure for feed barley.

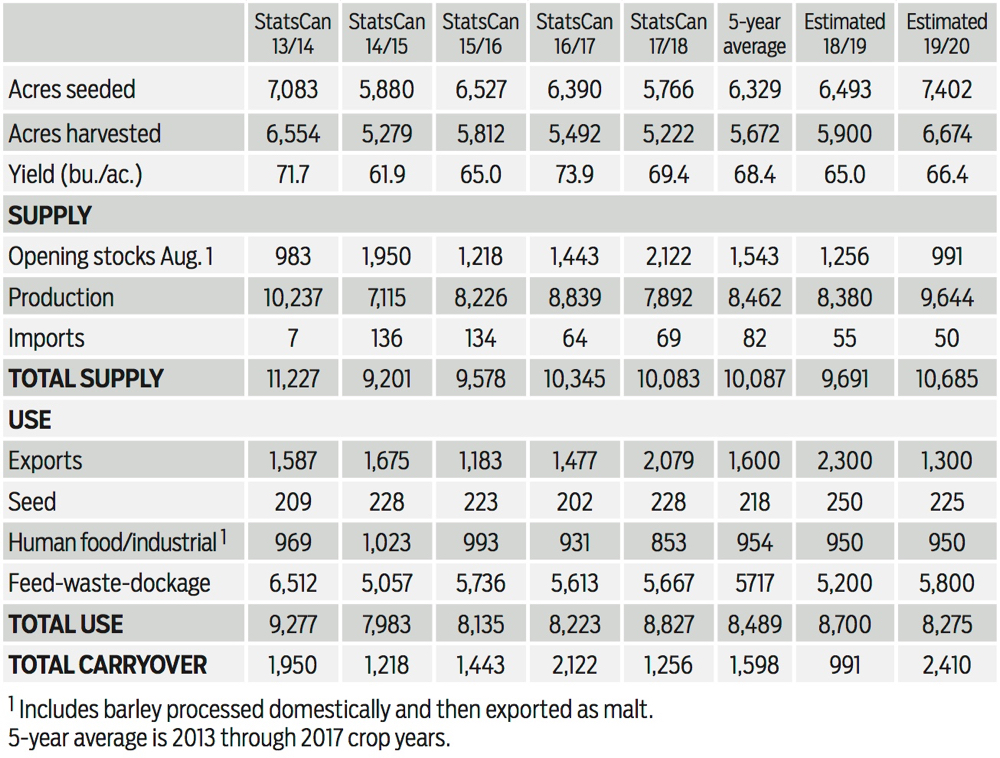

Statistics Canada released their July crop survey on August 28. The average Canadian barley yield was estimated at 66.4 bushels per acre, resulting in a crop size of 9.6 million mt. It’s important to stress that most traders feel the crop size is in the range of 10.0 million mt to 10.2 million mt. Statistics Canada is usually conservative on their first estimate. On the attached supply and demand table, notice that total supplies for the 2019-20 crop year are estimated at 10.7 million mt, up one million mt from the 2018 beginning stocks of 9.7 million mt.

Given the year-over-year increase in production, the function of the market is to encourage demand through lower prices. Hence, the $80/mt drop in market since midsummer. First, it is important to remember that all major exporters of barley experienced a year-over-year increase in production. European Union production is estimated at 60.3 million mt, up from last year’s drought-stricken crop of 55.9 million mt. Russian production is expected to finish at 18.5 million mt, up from 16.7 million mt last year, while the Ukraine crop is projected to come in at 8.7 million mt, up 1.1 million mt from the 2018 production. It’s a bit early but Australian production could reach up to 9.5 million mt, up from 8.3 million mt last year. There is stiff competition on the world market. Canadian barley exports for the 2019-20 crop year are estimated at 1.3 million mt, down from the 2018-19 exports of 2.3 million mt.

Read Also

Barley market poised to strengthen

Barley production below the 10-year average will cause prices to trade above their 10-year average, Jerry Klassen writes, noting the barley market cannot afford a 2026 crop problem.

Domestic seed usage and domestic processing is about the same every year. Notice that the five-year average usage for feed barley is 5.7 million mt. At this stage of the crop year, we’re factoring in average type of feed usage of 5.8 million mt. This implies very small imports of U.S. corn into southern Alberta. Adding up the supply and demand, the carry-out is projected to finish near 2.4 million mt, which is up from the 2018-19 ending stocks of 1.0 million mt and up from the five-year average carry-out of 1.6 million mt. As a rule of thumb, if the carry-out is above the five-year average, prices will be below the five-year average.

Outside influences are also negative for the feed barley market. At the time of writing this article, nearby Minneapolis wheat futures were near 10-year lows. Canadian non-durum spring wheat is expected to come in at 25.1 million mt, up from last year’s crop size of 23.9 million mt. Domestic feed wheat prices have been higher than elevator bids for export movement. Therefore, we’ll likely see a fair amount of wheat move into domestic feed channels in the first half of the crop year. The U.S. corn market experienced a sharp rally during the summer due to the uncertainty in production. It now looks like U.S. corn production will be higher than earlier anticipated; prices are expected to trend lower due to the year-over-year decline in U.S. domestic and export demand.

In conclusion, the year-over-year increase in Canadian barley production will keep the market under pressure for the 2019-20 crop year. Export demand will be down sharply so domestic demand will be the main driver of the price structure. Ending stocks will be above the five-year average resulting in prices trading below the five-year average.