Despite record-high prices for feeder cattle this spring and summer there appears to be no signal that the North American cattle herd has transitioned to the expansion phase. The heifers kept for breeding were down, as of July 1, while heifers for slaughter were up. Depleted feedstocks, record-high feeder cattle prices and widespread areas of drought in Western Canada worked in tandem to move more cattle into feedlots. Fed cattle prices remain strong. Total Canadian beef exports are expected to be lower in 2023, market share is expected to increase to Canada, U.S. and Mexico, but decline to Asia, the Middle East and North Africa. Replacement ratios are significantly higher compared to last year and last quarter.

Drought hits Canadian cattle herd again

The Canadian cattle herd continued to liquidate this year. The July 1 cattle inventories released by Statistics Canada show the total number of cattle and calves was down 1.5 per cent from last year’s revised 12.16 million head, as drought hit parts of Western Canada again during the 2023 grazing season. This is the smallest inventory since 1989. The beef cow inventory was also down 1.5 per cent to 3.66 million head. Beef heifers kept for breeding were down a significant 3.2 per cent to 600,900 head. Heifers that may have been kept for breeding early in the spring were moved to feedlots by mid-summer as dry weather settled in. As cow-calf pairs came to auction throughout the summer, they were split: calves moved to feedlots and cows sold. Canadian beef production for the remainder of the year will rely on feeder imports.

According to the Canadian Drought Monitor, most of Western Canada experienced some level of abnormally dry weather this summer. Only a small patch of central and northern Alberta received adequate moisture, as did the northeastern corner of Manitoba. However, most crop and grassland acres across the Prairies ranged from abnormally dry to severe drought. A significant portion of southern

Read Also

What to know before you go to Agribition 2025

If you’re attending Agribition 2025, this is the place to find out about tickets, dates and what’s happening this year.

Alberta and southwest Saskatchewan, as well as a small pocket south of Winnipeg, experienced extreme drought.

U.S. cattle herd liquidating

The U.S. cattle herd also continued its liquidation phase this year. The July 1 cattle inventories released by USDA reported total cattle and calves were down 2.7 per cent from last year to 95.9 million head. The U.S. beef cow herd is down 2.6 per cent to 29.4 million head, currently the lowest on record, going back to 1971. Beef heifers kept for breeding were 2.4 per cent lower than last year and were also the lowest on record. The total supply of calves and cattle outside of feedlots was down 3.6 per cent from last year. Smaller inventories outside of feedlots will continue to negatively affect domestic beef production into at least the first quarter of 2024. Year to date, the U.S. has been a net feeder exporter to Canada of about 61,000 head, but a net feeder importer with Mexico of over 650,000 head. Feedlot utilization rates and domestic beef production will be dependent on the movement of Mexican feeders into the U.S.

Canadian steer carcass weights trend heavier

Canadian steer carcass weights in the first quarter of 2023 averaged 933 lbs., four lbs. heavier than the first quarter of 2022, and a significant 13 lbs. heavier than the five-year average for the first quarter. A substantial transition occurred in the second quarter as steer carcass weights dropped to 885 lbs., 26 lbs. lighter than the second quarter of 2022 but only five lbs. lighter than the five-year average. The third quarter has once again seen weekly steer carcass weights climb over the five-year average. With carcass weights seasonally increasing, expect to see third-quarter carcass weights settle somewhere between last year’s large number and the five-year average.

Looking at the Canadian Steer Carcass Weight chart, this is largely how western Canadian carcass weights have been trending as Canadian averages are driven by the West. Eastern Canada looks significantly different. In the East, carcass weights have been at or above both last year and the five-year average since January. Even at their seasonal low in July, eastern Canadian steer carcasses averaged nine lbs. heavier than in July 2022 and 18 lbs. heavier than the five-year average for July.

The number of heifers in the fed slaughter mix remains historically high. From January to March 2023, heifers averaged 36 per cent of total fed slaughter, five percentage points higher than last year and three percentage points higher than the five-year average. However, from April to August, heifers made up 39 per cent of total fed slaughter, up from 35 per cent last year.

The percentage of Canadian cattle grading AAA or Prime in 2023 has shown improvements when compared to the five-year average but has struggled to keep up with last year.

The U.S. has consistently outperformed Canadian quality grading. U.S. carcasses grading Prime or Choice in 2023 are mostly steady with the five-year average, with 80-85 per cent of all carcasses making either Prime or Choice grade.

Fed production lower, non-fed elevated

Domestic beef production year-to-date is six per cent below a year ago at 1.9 billion pounds and is fully steady with the five-year average. The recent increase in steer carcass weights has not compensated for reduced fed slaughter numbers. Domestic fed production is eight per cent below last year and over one per cent below the five-year average at 1.6 billion pounds. Monthly fed production in 2023 has largely been below year-ago levels. The exceptions were January, as the last of the ample 2022 feedlot placements worked their way through the supply chain, and May when the price of fed cattle rocketed higher, pulling fed supplies forward. Non-fed production has remained elevated this year, nearly nine per cent higher than the same time last year, and 6.5 per cent higher than the five-year average at 264 million pounds. The increase in non-fed beef production has supported domestic beef production, though with lean trim and grinds, rather than high-quality steaks.

Canadian beef export destinations shift

From January to July 2023, beef and veal export volumes totalled 278,229 tonnes. The U.S. continues to be our largest market for beef and veal exports, Japan comes in second and Mexico third. South Korea and Vietnam round out the top five. Year-to-date export volumes increased to the U.S. (plus one per cent), Mexico (+34 per cent), Hong Kong and Macau (plus three per cent), and the European Union (+44 per cent), but declined to Japan (-37 per cent), Southeast Asia excluding Taiwan (-12 per cent), South Korea (-31 per cent), Taiwan (-30 per cent), and the Middle East and North Africa (-48 per cent). There were no exports to the U.K. or China. Export volumes this year are projected to be 3.3 per cent lower than in 2022 (nearly 494,000 tonnes).

The value of those exports, however, rose from last year. Year-to-date export values are up 1.4 per cent to $2.7 billion. The value of exports increased to the U.S. (+14 per cent) and Mexico (+41 per cent), but declined to Japan (-41 per cent), South Korea (-49 per cent), and Vietnam (-35 per cent).

Transportation costs, combined with softer beef demand outside of North America, has shifted market share. Regionally, Canada, the U.S. and Mexico are expected to increase their market share of Canadian beef. Asian countries, as well as the Middle East and North Africa, are expected to decrease their market share. The U.S. is projected to be a recipient of almost 73.7 per cent of Canadian beef exports this year, up three percentage points from last year. Mexico is projected to receive 7.2 per cent, a two-percentage point increase. Japan is projected at 9.7 per cent market share, down 3.5 percentage points from last year, and South Korea is projected at 3.7 per cent market share, down one percentage point.

Historically high fed cattle prices ease

Fed steer prices remained strong in 2023, though there has been some softening in the second half of the year. In June, fed steers in Alberta, Ontario and the U.S. peaked.

By August, there was a significant divergence between fed steer prices in Canada and those in the U.S. Canadian steer prices softened over five per cent, averaging $233/cwt, while U.S. fed steers strengthened over one per cent, averaging $247/cwt. September fed steer prices are expected to rebound in Canada and continue strengthening in the U.S. Strengthening momentum should continue right to the end of the year, using the live cattle futures as a guide. However, Canadian fed cattle prices in the fourth quarter will depend on basis, which transitioned from being strong in July (+$5/ cwt) to weak in August (-$8/cwt).

Canadian cull cow prices ease

Cow prices in both Alberta and Ontario tend to strengthen in the first half of the year and 2023 was no different. Alberta D2 cows crossed the $150/cwt threshold for the first time in history in May and maintained that momentum through the first half of the summer. Alberta D2 cows then ran into some headwinds in August averaging $149/cwt. Ontario D2 cow prices peaked in June at $142/cwt and have moved sideways through the summer. Since May, Alberta D2 cow prices have been 31-46 per cent higher than last year; Ontario D2 cow prices have been 20-26 per cent higher.

Feed grain prices support cattle margins

Lethbridge barley prices spent the first half of the year with little deviation from $420/tonne and averaged $417/tonne in August. Other feed grain prices fell since March, increasing their competitiveness. Since March, Great Falls barley has fallen 25 per cent to $152/tonne, Ontario corn is off 18 per cent at $259/tonne, and Omaha corn is down 20 per cent at $302/tonne. Since harvest began, barley prices have finally dropped to be closer to $360/tonne. There is no guarantee that barley prices will remain at this level, as the 2022 harvest season also saw Lethbridge barley prices plummet, but then climb a couple of months later. The drop in feed prices has been supportive of feeder prices and feedlot margins.

Calf prices roar higher

Alberta calf prices kept driving higher in the second half of 2023. Alberta 550-lb.-feeder steers began the year at $300/ cwt and have put in new weekly highs consistently since then. These mid-weight feeders climbed 25 per cent by August, averaging $375/cwt. Feedlots were placing these summer calves against the April live cattle futures that were consistently in the US$189-193/cwt ($253-258/cwt) range throughout August. By September, Alberta 550-lb. steers were closing in on $400/cwt.

Ontario 550-lb. steers had more trouble gaining traction in the spring after a strong winter. However, by late summer, these steers made up for lost time. Ontario 550-lb. steers averaged $382/cwt in September, a 31 per cent jump from April.

U.S. 550-lb. steers have shown no signs of slowing down, and have climbed 35 per cent since January, to average $378/cwt in August. Alberta 550-lb. steers have been priced at a $2-$15/cwt discount to U.S. 550-lb. steers since April.

The record-high prices received for feeder cattle this year have provided options for those cow-calf producers who may be short feed this fall. However, record-high prices do not guarantee profit. For those weighing the decision to liquidate some of their cows or purchase feed, average cow-calf margins in both Alberta and Ontario are estimated to be in the black and possibly among the largest in history. While feed costs remain elevated, higher margins may help encourage some producers to retain their cow herd this winter and reap those benefits with next year’s calf crop.

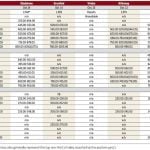

Replacement ratios increase

Replacement price ratios measure the price of a replacement animal purchased against the price received from an animal sold on a per-hundredweight basis. This ratio also plays an important role in profitability as more dollars required to pay for a replacement animal leaves fewer dollars available for other expenses and can reduce profit. In the third quarter of 2023, replacement ratios are six to 19 per cent higher in the West and nine to 13 per cent higher in the East, compared to the third quarter of 2022.

For the third quarter of 2023, replacement ratios increased nine to 14 per cent in the West and nine to 12 per cent in the East compared to the second quarter of 2023. The largest price ratio increases were seen on 400- 500-lb. heifers and 500- 600-lb. steers, with ratios increasing 11-14 per cent in the West and 11-12 per cent in the East. The price ratio on short-keep steers in the West also increased 14 per cent.

Despite higher replacement ratios, feedlot capacity in Alberta and Saskatchewan has continued expand- ing, indicating profitability in the sector. Feedlot capacity in Alberta and Saskatchewan is estimated to have increased by nearly one per cent from 2021 to 2022 according to the Canfax feedlot demographics survey. Risk management strategies have reduced debt exposure with lending institutions.