Alberta packers were buying fed cattle in the range of $150 to $152 FOB the feedlot during the last week of January. This compares to average values of $136 to $138 FOB the feedlot during the month of December. While prices have stabilized for the time being, there is a fair amount of uncertainty moving forward. At the time of writing this article, North America was at the height of the COVID-19 pandemic, which continues to influence overall beef demand. At the same time, the backlog of market-ready supplies appears to be coming to an end on both sides of the border.

Read Also

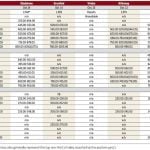

Cattle Market Summary

Break-evens, cow and calf prices, plus market summaries courtesy of Canfax and Beef Farmers of Ontario. Cost of Production September…

It’s important that cow-calf producers have a good handle on the fed cattle market to help time calf sales. Backgrounding operators also need to be aware that the fundamentals are changing. A small change in the fed cattle market tends to be amplified in the feeder complex. Producers need to be aware that their feeder cattle are the live cattle market five to nine months forward. For example, if you’re selling 550-pound calves in February, you need to know what fed cattle prices the finishing feedlot is facing in the final quarter of 2021. In this article, I’m going to provide an overview of the fed cattle and beef fundamentals for 2021.

The U.S. cattle inventory report was considered bullish for the fed cattle market. The U.S. 2020 calf crop was estimated at 35.1 million head, down from the 2019 calf crop of 35.6 million head. This is sharply lower than expectations from the semi-annual cattle inventory report released last July. The Canadian calf crop for 2020 is expected to come in near 4.2 million head, down 50,000 head from 2019. We’ve seen two consecutive year-over-year declines in the U.S. calf crop and three consecutive declines in Canada. Lower calf crops equal lower feedlot placements equals lower beef production.

Fed cattle supplies will tighten in the second quarter of 2021 on both sides of the border. Last year was unique, to say the least. The lower slaughter pace in the second quarter resulted in a backlog of market-ready supplies in Canada and the U.S. We’ve seen lower placements on both sides of the border on the last few cattle-on-feed reports. Without going into detail, it appears that the U.S. backlog of market-ready supplies will be cleaned up by the end of February. In Western Canada, it looks like feedlots will be more current with production during April or May. I don’t expect the fed cattle set-aside program to be used after March.

In the table below we have the quarterly beef production estimates. Notice the most burdensome supply situation was during the third quarter of 2020. Supplies have been tightening since then. The USDA is forecasting second-quarter production to finish near 6.760 billion pounds. While this is up from last year, it’s down from the 2019 second-quarter output of 6.814 billion pounds. Third quarter production for 2021 is projected to reach 6.825 billion pounds, which is also below 2019; however, with the lower calf crop on the last inventory report, this may be on the high side. I’m looking for the USDA to provide a haircut to the third-quarter output on subsequent USDA WASDE reports. I want to draw attention to the fourth quarter of 2021. Notice production is expected to finish near 6.750 billion pounds. This is the lowest fourth-quarter output since 2017.

Beef demand is inelastic; a small change in supply has a large influence on the price. Second, a one per cent increase in consumer spending equals almost a one per cent increase in beef demanded. There were approximately 10 million Americans unemployed at the beginning of January due to the COVID-19 pandemic. Approximately two-thirds of these workers should be back at work by July. In the meantime, the U.S. and Canadian government aid packages are bridging the income for the unemployed until the economy returns to normal. In any case, there is potential for a demand surge during the summer time frame. Consumer spending will improve in the latter half of 2021.

What does all this mean for the feeder cattle market? Yearlings are expected to trade sideways over the next couple of months because projections still show larger supplies during the summer. Lighter calves and grassers are expected to percolate higher because these cattle will come on the fed market in late fall or winter. Look for grass cattle prices to make fresh 52-week highs during the spring. During the fall period, yearlings fresh off grass could also make fresh annual highs.

The most profitable period for cattle producers is when the U.S. economy moves into expansion after a recession. Prices are further enhanced by the contracting cattle herd. Sounds a bit like the history between 2012 and 2015. The next two or three years will be a very profitable period for the cow-calf producer.