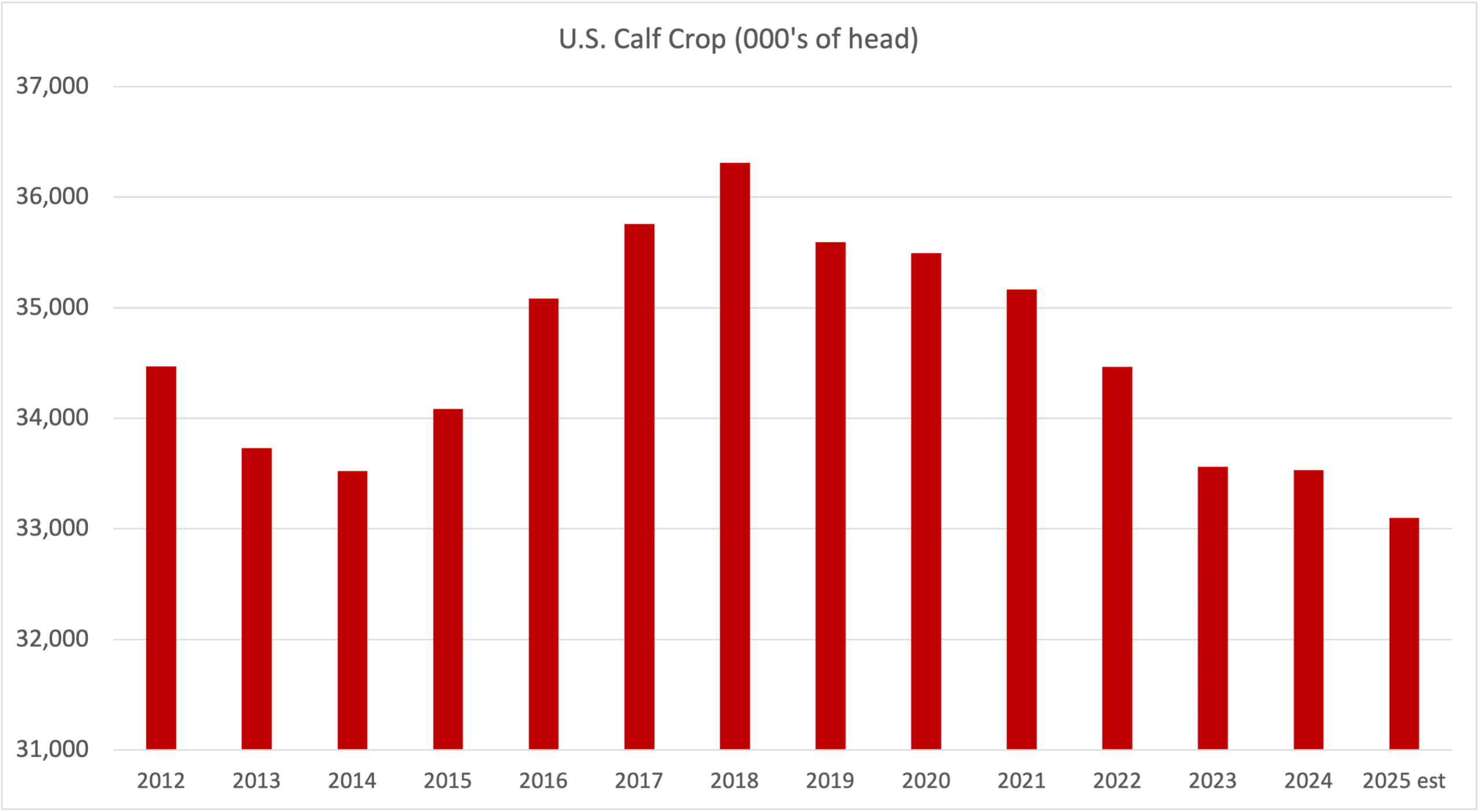

Once again it is that time of year when I receive many inquiries from cattle producers with regard to the price outlook for feed grains. At the time of writing this article, Lethbridge area feedlots were buying feed barley in the range of $218/mt to $223/mt; however, feedlots located between Calgary and Edmonton were making purchases from $205/mt to $210/mt.

The market has been functioning to attract farmer selling in the two main price discovery regions of Western Canada. Available supplies are rather snug moving into road ban season and spring seeding. The sharp year-over-year decline in production, along with the higher quality crop, has set a firm tone throughout the winter. Approximately 50 per cent of the 2017 crop was malt quality and farmers with malt supplies do not want to sell into feed channels. In this article, I will discuss the price outlook for feed barley and some of the factors that will influence the price structure over the next four to six months.

Read Also

Factors influencing cattle feeder market during the fall of 2025

Market analyst Jerry Klassen weighs in on live cattle markets

Statistics Canada’s final production estimate came in at 7.9 million mt, which is down from the 2016 crop of 8.8 million mt and down from the 10-year average of 9.0 million mt. While yields turned out better than anticipated, lower seeded acreage was the main factor resulting in the year-over-year decline in production. Of the 7.9 million mt of production, industry estimates suggest that as much as 50 per cent or 4.0 million mt was malt quality. Given the tighter feed barley supplies, the function of the market is to ration demand through higher prices. The market needs to trade higher to shut off exports and encourage the use of alternate feed grains such as corn. Also, by the end of the crop year, some of this malt-quality barley needs to flow into feed channels.

While production was down from 2016, the demand is stronger than year-ago levels. For the week ending January 18, crop year-to-date exports were 890,000 mt, which is up from year-ago exports of 467,000 mt. Most of the exports are malt-quality barley and these sales were made earlier in the crop year. At the time of writing this article, Russian feed barley is offered at US$195/mt fob the Black Sea while Australian barley is quoted at US$223/mt fob the West Coast. Canadian feed barley is uncompetitive on the world market due to higher prices in the domestic market. The market has accomplished this function by shutting off exports. Fresh malt barley sales are also unlikely because of strong competition from Australia and other major exporters. China has been actively buying Black Sea feed barley and Australian barley for malt purposes.

During the 2016-17 crop year, there was a significant amount of feed durum and feed wheat that was used in Western Canadian feedlots. However, approximately 95 per cent of the 2017 wheat and durum crops graded in the top milling category. Therefore, we’re seeing more barley used in feedlot rations.

There is a fair amount of Manitoba and U.S. corn flowing into southern Alberta. The barley market is accomplishing the function to encourage the use of alternate feed grains by trading at equivalent or higher prices than imported U.S. corn. However, we need to see more imports by the end of the crop year. In the major feeding regions of Alberta, feed barley prices are higher than malt barley. Most of the malt barley exports are flowing from Saskatchewan where the feed price remains at a discount to malt barley. This will change by the end of year because we’ll likely see the feed price in Saskatchewan higher than elevator bids for malt barley.

I’m forecasting a Canadian barley carry-out of 1.4 million mt, which is down from the 2016-17 ending stocks of 2.1 million mt and also below the 10-year average of 1.7 million mt. This suggests that the barley market needs to encourage acreage this spring, otherwise the feed barley supplies will be extremely tight for 2018-19. Given the tighter carry-out, the market will be extremely sensitive to growing conditions. Much of Western Canada has received less than 40 per cent of normal precipitation over the winter. Drier years are usually followed by dry years.

Outside influences are also supportive for the barley market. The Argentine corn crop is coming in lower than anticipated due to dry and hot conditions during pollination. U.S. corn is now competitive on the export market. Crude oil prices remain near three-year highs resulting in stronger ethanol demand. Earlier in winter, analysts were expecting a year-over-year decline in U.S. corn acres of three to six per cent, and this is also supportive of the overall feed grains complex.

In conclusion, feed barley prices have potential to rally $15 to $20/mt through the spring and summer. Feed barley prices will be highly correlated with corn values because of the substitution effect. By the end of the crop year, farmers with malt barley will be selling into feed channels limiting the upside.