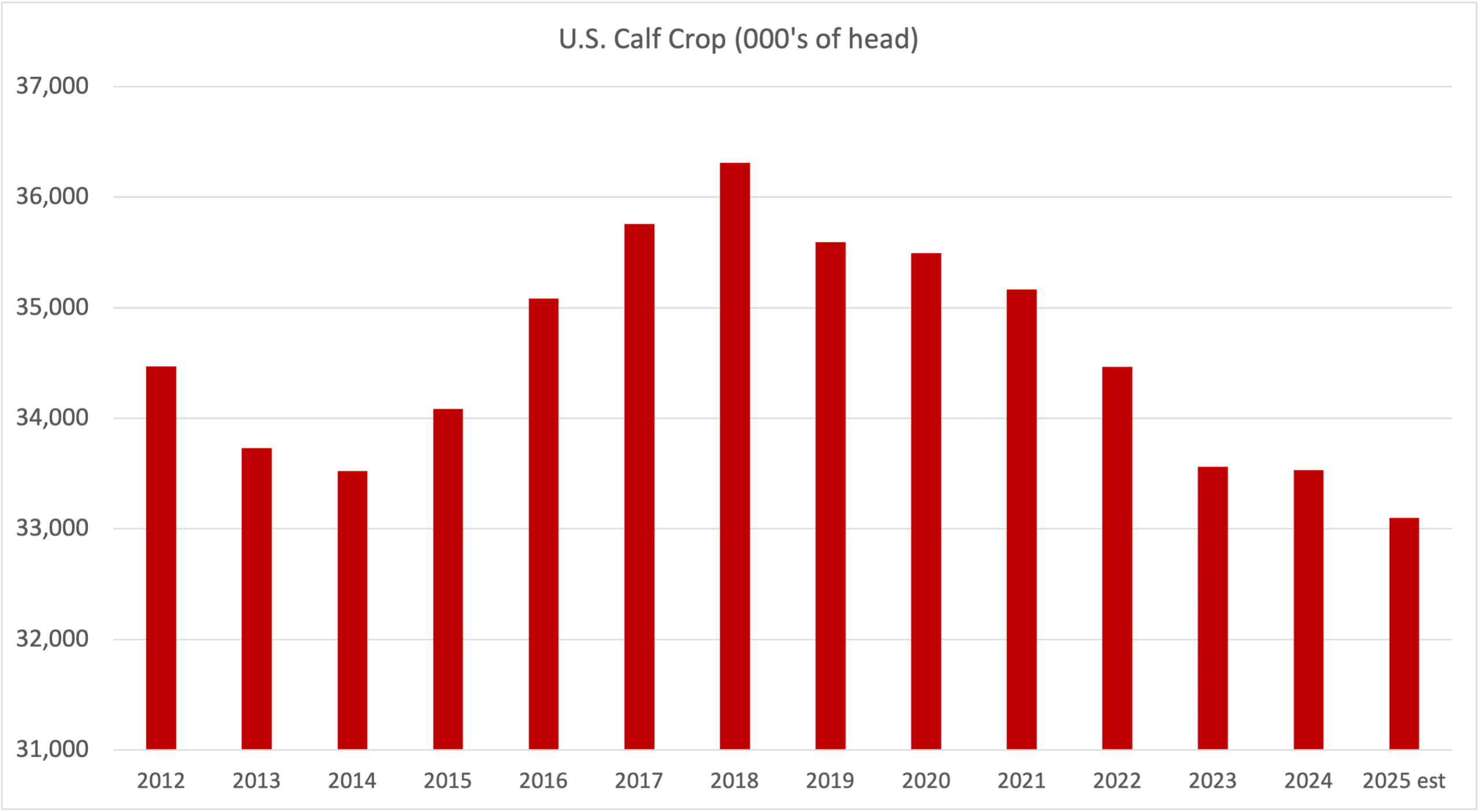

Barley and corn prices have been trading near five-year lows throughout the spring and summer. Despite the year-over-year decline in Canadian barley and U.S. corn acres, optimal weather has resulted in trend yield projections on both sides of the border. Production will be down from year-ago levels for both barley and U.S. corn crops; however, the fundamentals are rather tight for barley whereas the U.S. corn market is functioning to encourage demand.

I’ve received many calls from cattle producers over the past couple of weeks asking if they should be aggressive on barley purchases during harvest. Therefore, in this article, I’m going to discuss the Canadian and U.S. feed grain outlook for the 2024-25 crop year. Feeding margins are quite snug given current yearling prices. The cattle industry is banking on lower-priced grains which will be supportive for feeder cattle.

RELATED: Feed Weekly: More grain to enter feed markets

Read Also

Factors influencing cattle feeder market during the fall of 2025

Market analyst Jerry Klassen weighs in on live cattle markets

Canadian farmers seeded 6.386 million acres of barley this past spring according to Statistics Canada. Using a traditional abandonment rate and yield of 71 bu./acre, production has the potential to finish near 8.9 million tonnes, unchanged from last year and similar to the five-year average. Total supplies, which includes the carry-in stocks, are estimated at 9.6 million tonnes, down from the 10-year average of 10.2 million tonnes. Exports for the 2024-25 campaign will likely finish around 2.3 million tonnes due to the stronger demand from China. Australia’s exports will be lower in 2024-25. China tends to make their purchases during August which sets the price structure for exports for the total crop year.

We’re forecasting 2024-25 barley carryout near 1.3 million tonnes which is up from the 2023-24 ending stocks of 609,000 tonnes and similar to the 10-year average figure of 1.2 million. The reason we have domestic feed usage at 4.9 million tonnes is that we’re expecting 3.5 million tonnes of U.S. corn to trade into Western Canada. Imports of U.S. corn during the 2023-24 crop year will likely just finish under three million tonnes.

U.S. corn production is expected to finish near 15.1 billion bushels, marginally lower than the 2023 output of 15.3 billion bushels but sharply above the five-year average of 14.4 billion bushels. Total corn supplies are expected to reach 17 billion bushels, up nearly 700 million bushels from the five-year average. The market will function to encourage demand. Without going into details, the corn carryout will likely finish near 2.1 billion bushels, up from the 2023-24 ending stocks of 1.89 billion bushels and above the five-year average of 1.8 billion bushels.

A simple rule of thumb is that if the corn carryout is above the five-year average, corn prices drop to the five-year lows. In the 2019-20 crop year, corn futures traded in the range of $3.50-$4/bushel. Lethbridge barley was trading from $230-$260/tonne delivered. We expect to see aggressive offers of U.S. corn into Alberta once the U.S. corn harvest is in full swing.

Another caveat to consider is Western Canada will likely have a large volume of feed wheat. In past years, milling wheat traded into feed channels but in 2024-25 there will be about six million tonnes of feed wheat production in Western Canada. This will be due to sprouting or fusarium. This must saturate domestic feed demand or trade at very low prices to South Korea at similar values to U.S. corn. There are only a couple of possible homes for this wheat offshore.

In conclusion, we’re expecting about 3.5 million tonnes of U.S. corn to trade into Western Canada. There is potential for a large volume of actual feed wheat production. The U.S. corn carryout will finish above the five-year average causing barley and corn prices to trade near five-year lows. Chinese demand will set the price floor for barley in the non-major feeding regions of Western Canada. This feed grain environment is supportive of feeder cattle prices throughout the fall and winter.