Alberta fed cattle prices reached up to $275 on a dressed basis during the first half of January but have since come under pressure. At the time of writing this article at the end of January, Alberta packers were showing bids in the range of $262 to $265 delivered. April live cattle futures reached contract highs of $128.55 on December 16 but have since dropped to the $120 area heading into February.

We always say that the market moves, and then the media headlines come out to justify the recent changes in the market. Fears about the Chinese coronavirus have caused fear that beef demand and exports will be lower than earlier anticipated. At the same time, Bloomberg reports that government and academic experts in the U.S. have developed an effective vaccine against African swine fever. In any case, these are considered “Black Swan” type variables influencing the market swings from day to day; however, it’s important to look at the cattle and beef fundamentals as we move into the second and third quarters. You’ll find that the true fundamentals usually prevail. Second, you have to remember that packers are always working their margins two to six months forward, even though they are buying cattle in the spot positions for immediate or nearby delivery.

Read Also

Factors influencing cattle feeder market during the fall of 2025

Market analyst Jerry Klassen weighs in on live cattle markets

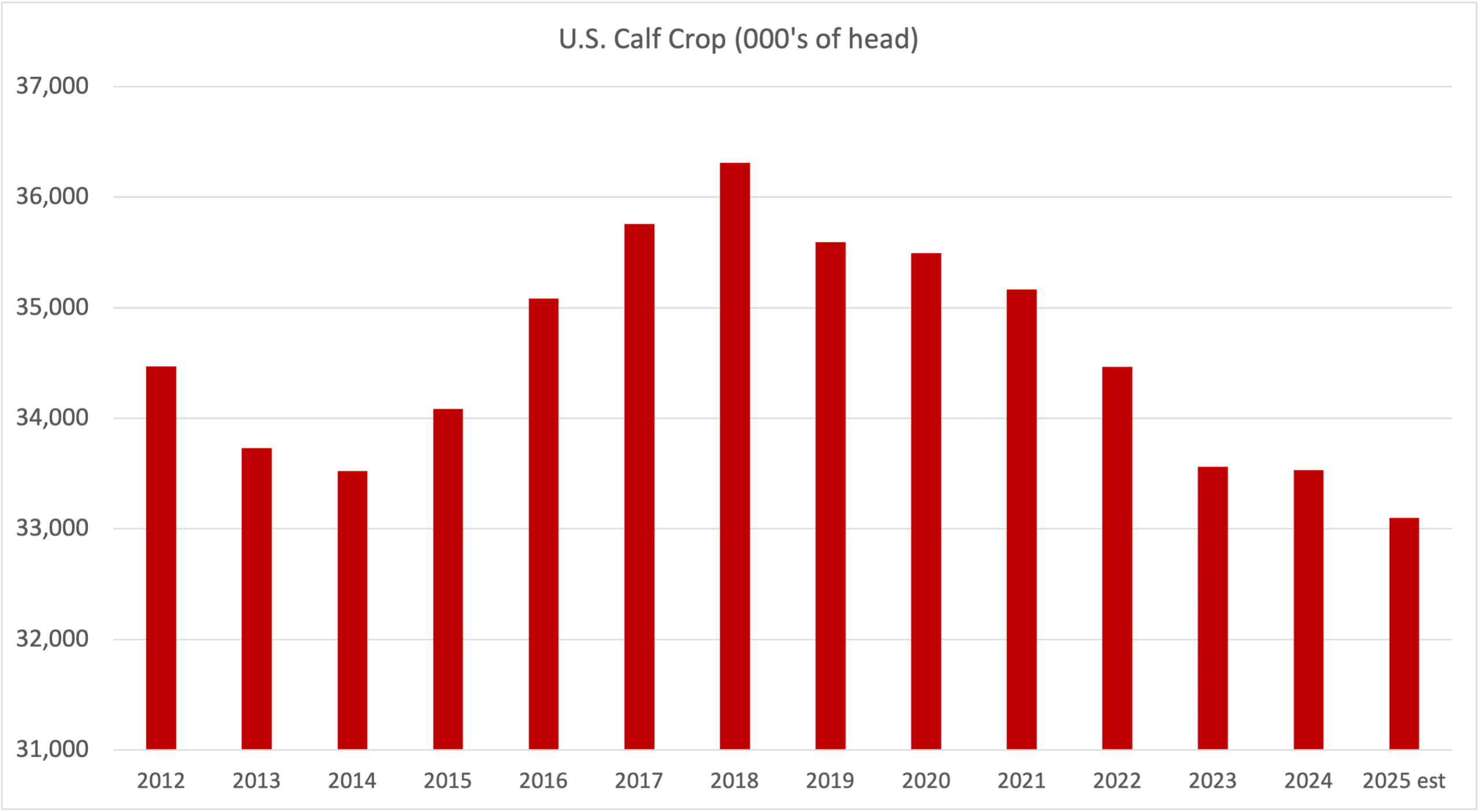

According to the USDA, the number of cattle on feed for slaughter in the U.S. as of January 1 totalled 11.958 million head, up two per cent from the January 1, 2019 number of 11.690 million head. U.S. feeder cattle placements during December 2019 were 1.828 million head, up three per cent from December of 2018. There is no doubt that there are a fair number of cattle on feed. More importantly, it’s important to realize that U.S. feedlot placements from September through December 2019 were 8.476 million head, up from 8.036 million for the same four-month period of 2018. The question is when will these cattle come on the market.

If we look at the U.S. placements by weight category, the bulk of these placements will come on the market during the second quarter. The USDA is forecasting second-quarter beef production to come in at 7.140 billion pounds, up 326 million pounds from the second quarter of 2019. Just as important, notice that 2020 second-quarter production is up a whopping 645 million pounds from the first quarter. The market is moving from a rather tight supply situation to an extremely burdensome environment within a three-month period.

In Canada, the placement structure is looking very similar. The Canfax cattle-on-feed reports had placements in Alberta and Saskatchewan from September through December 2019 at 1.089 million head, up from the same four-month period of 2018 when placements were 0.902 million head. Placements during September through December 2019 were up nearly 187,000 head over 2018.

If we look at the placements by weight category, market-ready supplies during May and June combined in Alberta and Saskatchewan could be up 140,000 head over May and June of 2019. The Western Canadian fed cattle market will function to encourage demand through lower prices.

Without going into detail, beef demand is rather inelastic. A small change in supply has a large influence on the price. During the summer months, beef consumption increases but this is also a function of lower prices.

What does this mean for the fed cattle market? It appears that packers have over half of their fed cattle requirements on the books for the first quarter and the market is focusing on second-quarter fundamentals. Beef production will experience a sharp year-over-year increase on both sides of the border. Feedlot margins have been positive during January but we’ll likely see profitability erode during the April through June timeframe. Yearling prices are expected to deteriorate over the next month because these replacements will come on the fed market during the summer months.

Once we move into the latter half of 2020, the fed cattle market will experience a similar pattern to last year. Beef production will likely be slightly below year-ago levels during the third and fourth quarters of 2020.

Market commentaries may be touting the coronavirus, and vaccine for the African swine fever; however, packers and merchants know that the main factor driving the drop in the cash and futures market is the burdensome beef supply scenario for the second quarter. Major cattle producers have also seen this coming and been aggressive with sales in the spot market and actively forward contracted or hedged up their fed cattle marketings in the May through December timeframe.