At last there are clear signs of beef herd expansion in Canada!

In 2015 the output, or productive capacity of the national herd was reduced: almost 13 per cent in numbers of animals marketed and 10 per cent in tonnage. Most of that reduction, however, is explained by an almost 20 per cent decline in heifer marketings and a 16 per cent decline in cow marketings. Inasmuch as dairy cow culling rates are quite stable one can be confident that all of the decline in cow marketings was out of the beef herd so I have recalculated the decline in beef cow culling to be 21 per cent. This is quite conclusive evidence that the long decline in the beef breeding herd has at last ended. The heifers that did not appear in the market in 2015 had obviously been retained from the 2014 calf crop and were bred in the summer of 2015. Alas their calves will not reach market until 2017, but one can be quite confident that the long decline in the national herd has been ended and growth has begun.

As stated often before, a decline in cow marketings is not, in itself, a sign of herd growth. Herd growth can only come from an increase in heifer retentions that exceeds the rate of cow culling. In 2015 approximately 800,000 fewer heifers were marketed than steers and were therefore available for herd replacements. The total cow cull was approximately 600,000 head. Since dairy cow marketings make up about 40 per cent of total cow marketings that means that only about 360,000 beef cows were culled in 2015. That’s a culling rate of about nine per cent, close to the lowest possible practical culling rate.

The data above suggests a very vigorous growth rate with 800,000 replacement heifers replacing 360,000 culled beef cows. Bump that up to about 400,000 to allow for natural death loss in the breeding herd. However, two other factors must be taken into consideration. The first is that the fed cattle slaughter includes a sizeable number of dairy steers and very few dairy heifers. Also my estimate is based on the assumption that heifers and steers in the export data were present in the same ratio as in the domestic kill and this may not be the case. Reliable data on the sex of exported fed and feeder cattle is difficult to find. So, if we allow for 200,000 dairy steers, based on an estimate that I have made, and assume that exports of feeder and slaughter cattle were equally divided between steers and heifers, the spread between steers and heifers marketed would be reduced to about 525,000 head. That suggests a net increase of 125,000 beef cows or a beef herd expansion rate of 3.1 per cent. A more conservative estimate is that the beef breeding herd has expanded by 2.5 to 3.0 per cent. I’ll stand by that estimate for 2016 and we will see what the inventories show.

Read Also

Body condition, nutrition and vaccination for brood cows

One of the remarkable events of the past century related to ranching has been the genetic evolution of brood cows….

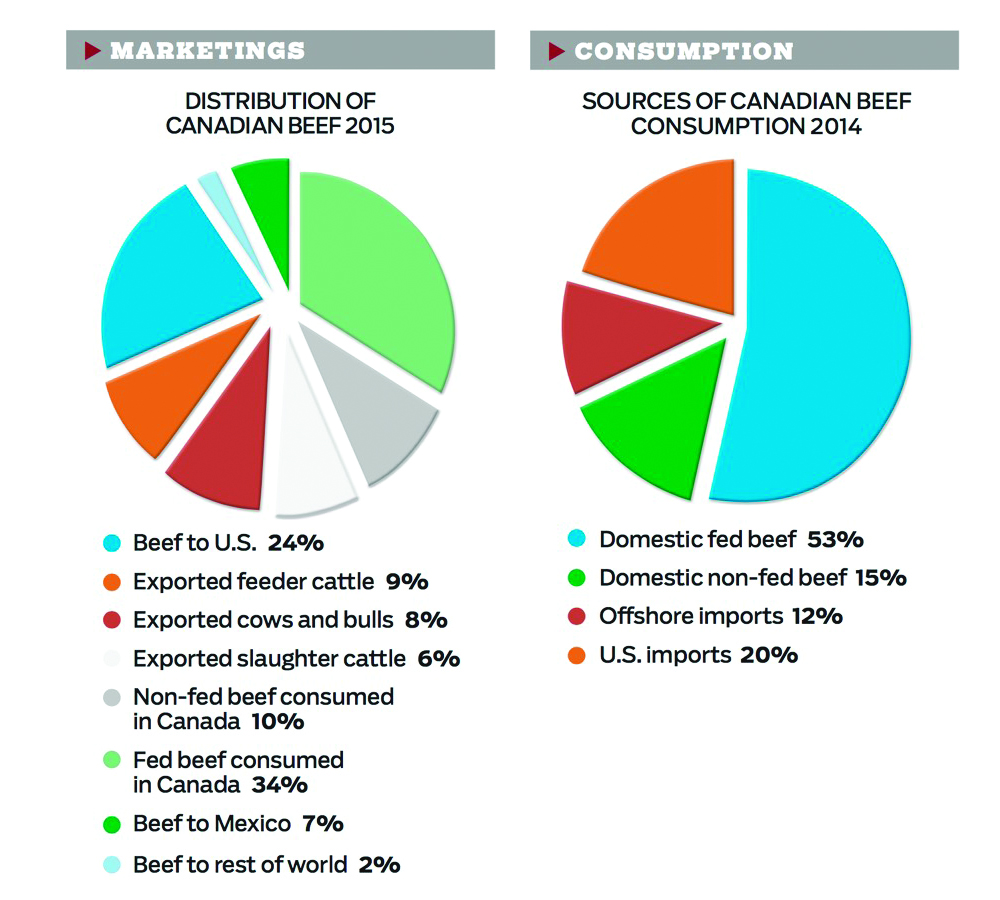

The declining supply led to a 5.3 per cent decline in domestic slaughter but a much larger 32.4 per cent decline in slaughter cattle exports and a 31 per cent decline in feeder cattle exports.

Despite a decline in overall supply, total beef exports remained unchanged. However, exports to the U.S. increased 5.3 per cent while exports to Mexico and to offshore markets declined 12 per cent. Beef imports rose but only slightly, declining 4.0 per cent from the U.S. and rising 12.4 per cent from offshore for an overall increase of 1.4 per cent.

In 2015 per capita beef consumption has taken the sharpest drop in many years to 17.7 kg per capita on a retail weight basis. That converts to 24.2 kg (53.4 lbs.) on a carcass basis. Per capita consumption or disappearance is now lower than it has been since the mid-1950s.

The industry in Canada has been much slower than the U.S. in commencing herd growth.

Note: The numbers in this analysis that relate to weight are all expressed as “retail weights” which are 73 per cent of carcass weights. I did this to bring domestic production in closer alignment with beef imports and exports. This conversion factor of 73 per cent is used to convert per capita consumption from a carcass weight to a retail weight basis.

Charlie Gracey is an industry analyst living in Ontario.